Thinking about filing your taxes but feeling confused? That’s alright, because we’ve got all you need to know about your taxes without the help of a CA. You can do your own calculations, and feel the accomplishment once you’re done.

Here are some important aspects to know your taxable income.

Income Categories

The total income of the assessee is divided into five heads:

- Income from salaries

- Income from house property

- Profit and gain of business or profession

- Capital gains

- Income from other sources

If your income falls under any of these heads, it is chargeable to tax under the Income Tax Act, 1961.

When does tax need to be paid?

If your income, from any of the above heads, exceeds the maximum exempt amount, it will be charged to tax based on the tax slabs specified by the Government. Taxability status also depends on the residential status of the assessee.

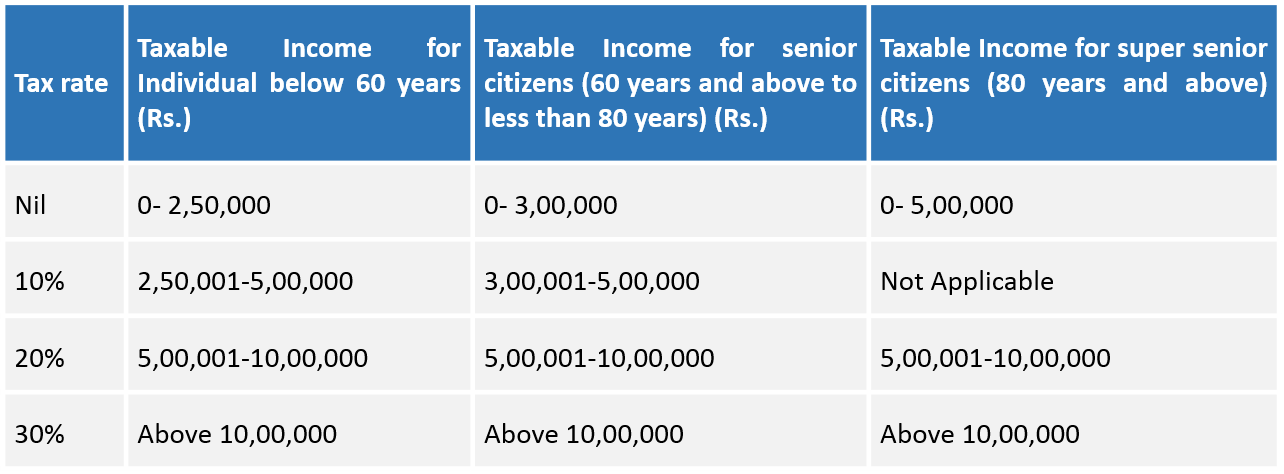

Tax slabs in India for different categories

Income tax slabs differ depending on the type of the assessee. The assessee can be an individual (aged below 60 years, senior citizen, super senior citizen), co-operative society, firm, local authority, domestic company or any other company.

The slab for an individual below 60 years also applies to Non Resident Individuals, Hindu Undivided Family, Association of Persons, Body of Individuals and Artificial Judicial Persons.

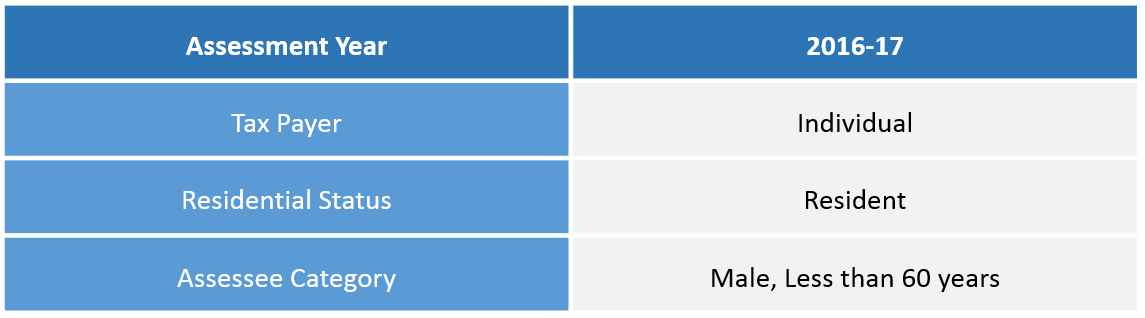

Given below are the tax slabs for an individual resident below 60 years (both men and women), senior citizens (individual aged between 60 years and 80 years) and super senior citizens (individual aged above 80 years) for the Assessment Year 2016-17 (i.e. Financial Year 2015-16):

Additional Read: How to Choose the Perfect Income Tax Return Form for You

In addition to the tax slabs given above, the assessee is also required to pay surcharge at the rate of 12% of the Income Tax (if the income exceeds Rs. 1 crore), education cess (at the rate of 2% of the total income tax and surcharge) and secondary and higher education cess (at the rate of 1% of the total income tax and surcharge).

Tax deductions

Once you arrive at the total income, you can avail a few deductions to arrive at the net taxable income. As the name suggests, deductions are a reduction from your total income, which helps in reducing your tax liability. There are various sections under which you can claim deduction.

Section 80C: The most popular section under the Income Tax Act used to claim deductions is Sec 80C. Life insurance premium payment, contribution to provident fund, payment for annuity plan, repayment of principal of home loan, investment in 5 year fixed deposit with bank, tuition fees paid for children and contribution to a notified pension fund are some avenues where you can claim deduction under Sec 80C. The maximum deduction that can be claimed under Sec 80C is Rs. 1.5 lakh.

Additional Read: Nifty Tax Savings from Investing in Property

Other Sections: Some other popular sections under which you can claim deduction are Sec 80D (payment of medical insurance premium), Sec 80G (donations made), Sec 80CCD (NPS contribution), Sec 80E (interest payment on education loan) and Sec 24b (interest payment on home loan).

One should refer to the Income Tax Act to explore the various deductions available, the maximum amount that can be claimed, as well as other applicable conditions in order to reduce tax liability.

Additional Read: How to Whip Up Delectable Tax Savings

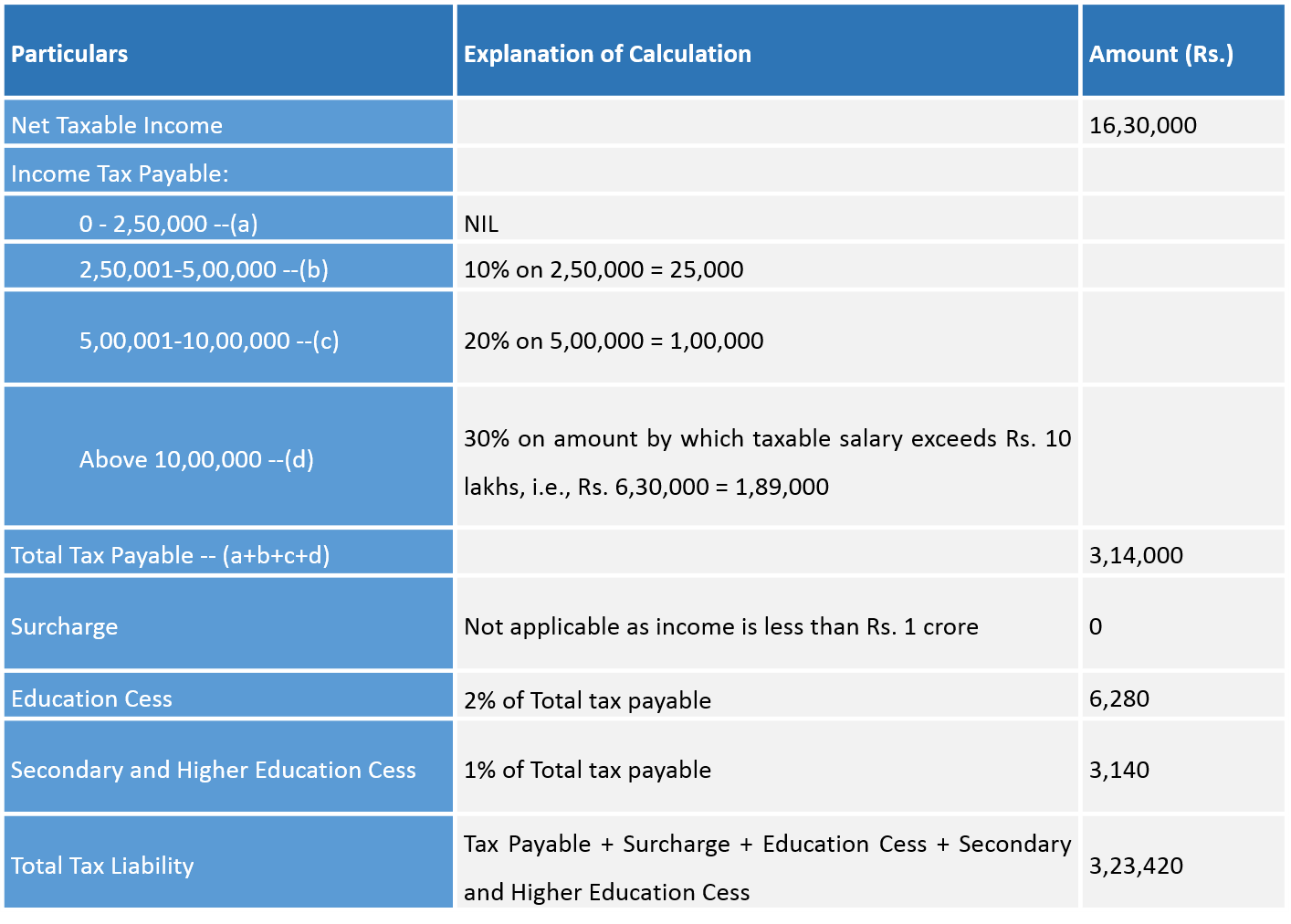

How much tax should you pay?

Tax computation can be quite tricky, especially if you are not aware of the underlying rules.

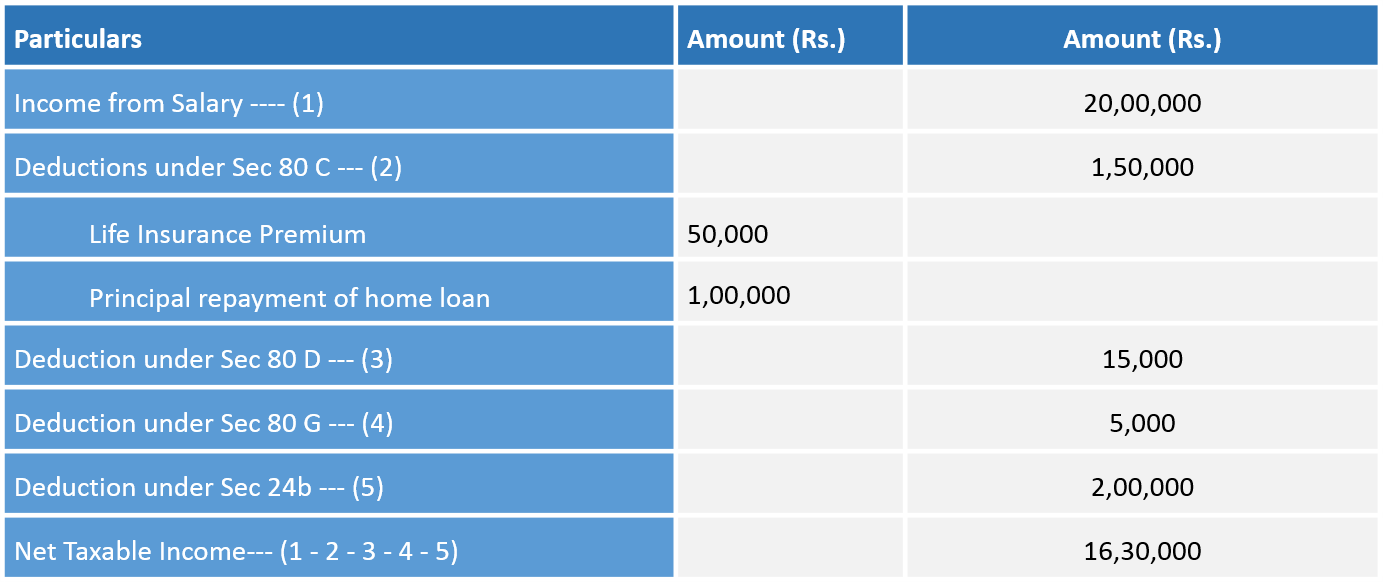

Let us take the case of Pankaj to understand how tax liability is computed. Let us assume that Pankaj earns a total salary of Rs. 20,00,000 in the Financial Year 2015-16 (i.e. Assessment Year 2016-17). He has no other income sources.

The following are his investments and payments during the year for the purpose of computing deductions:

- Payment of life insurance premium: Rs. 50,000,

- Principal of home loan repaid: Rs. 1,00,000,

- Medical Insurance premium: Rs. 15,000,

- Donations to notified charitable institutions: Rs. 5,000

- Interest of home loan paid: Rs. 2,00,000.

Calculation of net taxable income:

Other factors:

Income Tax Calculation:

Filing your taxes doesn’t need to be as painful as it seems.