Have you found yourself in this situation? You apply for a personal loan and are rejected!

Have you found yourself in this situation? You apply for a personal loan and are rejected!

You are stumped. How could this be? You’ve got everything in order and you know you have a credit history that the bank can check.

It’s not all about getting to the finish line but also how you got there!

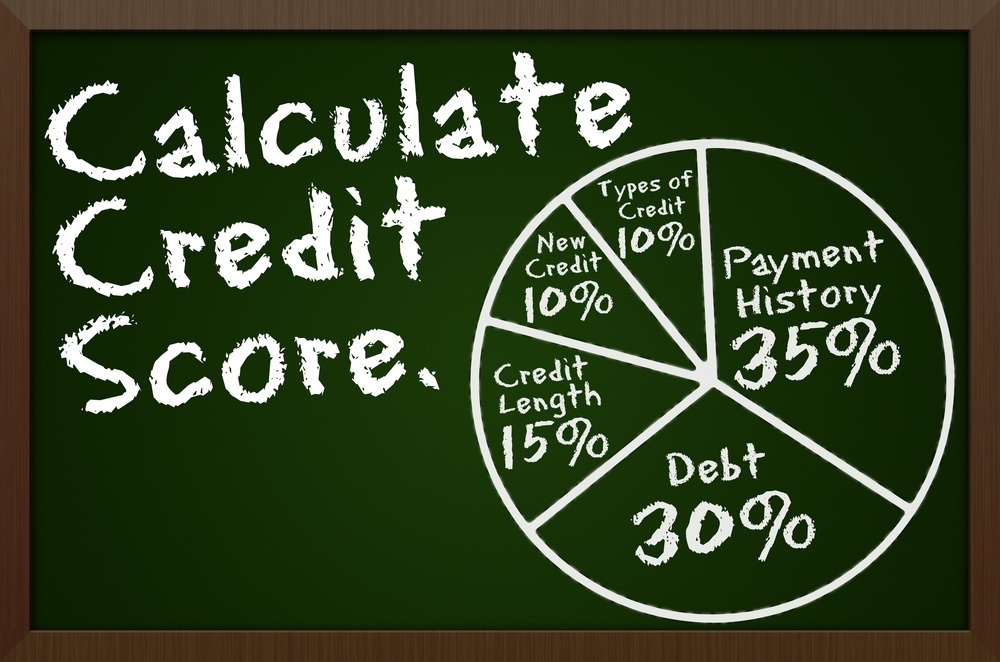

One big reason why you could be denied a loan is that even though you do have a credit history driving a good credit score (or so you thought), it probably looks like it collided head-on with a truck (a head-on collision with a truck is never a good thing). Result? A crumpled credit score.

Let’s say you did fulfil all your obligations but some defaults or late payments crept in due to unforeseen circumstances or poor decision making. Or, maybe you just didn’t know that there was more to it than just clearing debt.

You’re not alone. Many can’t imagine for the life of them why they would have a bad credit history. The reasons could be aplenty.

But, despair not! There are easy fixes that will take your crumpled credit history and remodel it to look like a shiny new Aston Martin!

Tips to recover from bad credit history

Be on-time

If you have let payments in the past go unpaid beyond the due date, pull your socks up and don’t let any more payments lapse. Ensure that you clear dues promptly and in full. If your credit history has soured because of delays, being regular will definitely help in improving it.

Keep your borrowing to a minimum

Let’s say you have a credit card with a limit of Rs.50,000. Try your best to not use more than Rs.35,000. If you come too close to the upper limit on your card, too often, it is viewed negatively as poor financial management, affecting your credit score adversely.

Pay all bills

It may seem insignificant but paying all your bills regularly, on time, and without conflict will go a long way in building a strong financial reputation and improving your credit history. This habit indicates to creditors that you are financially responsible, which helps offset a bad score.

Don’t keep transferring balances

It may sound very helpful to transfer your credit balance from one bank to another to either pay off debts or avail lower interest rates, but if you do it too often it’s going to work against you as you run the risk of being seen as flippant. Avoid this by researching the most affordable debt product for you both in the short and long run, transferring only if you find a markedly better deal elsewhere.

Undoing a ‘Residence Blacklisted’ status

Let’s say you just moved into a new house and applied for a loan. You may end up being rejected because the person who lived there before you had a bad credit history and the address is associated with them. It may feel like you are paying for the sins of others but redemption is not far off either. Simply continue to maintain a good credit history and sending a letter to CIBIL and other credit reporting agencies to inform them of the situation.

Don’t Cancel All Your Credit Cards

Cancelling all your debt to avoid bad credit ratings is not advisable. Even though they seem like harbingers of financial evil, if you cancel your cards you will be in a situation where you won’t have current credit to build any kind of credit history with. Keep the card, but use it wisely.

Once things start looking up and your credit history starts making you look like a financial saint, pull out all stops to not damage it again.

After all, if you do get it looking better than an Aston Martin… Well, okay, there is nothing more beautiful than an Aston Martin… but you get the drift!

YOU MAY ALSO WANT TO: Find out how much your current personal loan is costing you – Calculate Your EMI