Mimi Parthasarathy, Managing Director, Sinhasi Consultants Pvt Ltd

In India, Employee Provident Fund (EPF), commonly known as PF, is one of the best TAX-FREE debt investments for retirement. In “old school” employment situations, your PF accumulation was basically your retirement corpus. Nowadays, there are equity-linked schemes that have entered the market which give you an easy option to save for long durations of time.

We have noticed that since PF accumulation happens automatically as a salary deduction, and since withdrawals are also restricted, some of the best accumulations in PF are with those who have stayed in the same job for 15 to 20 years continuously. With the increments in salary, the contributions have also increased and this saving is actually a sizeable corpus and contributor for retirement.

Nowadays, trends are changing and there is high turnover in employment – this actually comes in the way of long-term savings in retirement-related funds and continuity in PF sometimes gets lost. We believe it is an important ‘must-have’ in your long-term portfolio. Below are some reasons that’ll show you exactly why.

It’s a retirement-benefit scheme that is available to all salaried employees (i.e people working in Government, Public or Private Sector Organizations). It’s a savings platform that helps them save a portion of their salary every month for retirement.

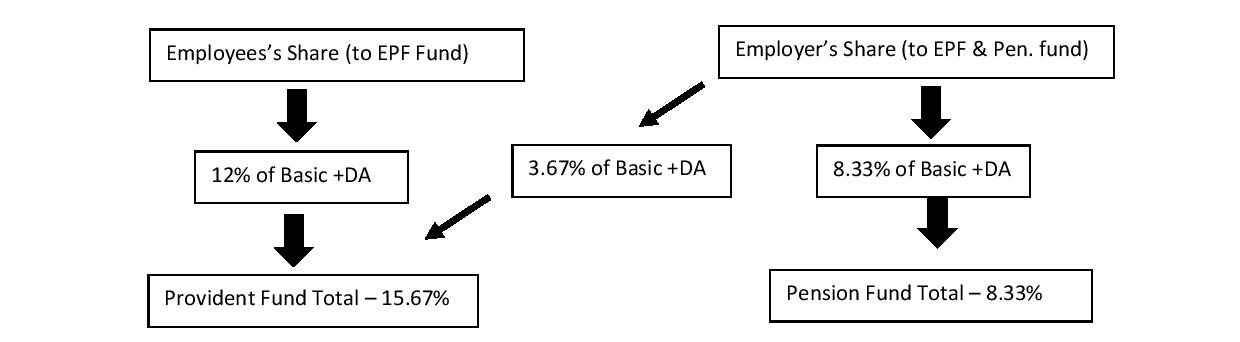

How Does It Work?

Interest Rates

The EPF interest rate of India is decided by the central government with the consultation of the Central Board of Trustees. While your contributions are made monthly, the interest is compounded yearly. The interest is paid on the amount standing to the credit of the employee on the 1st of April every year. This interest is added to the investment in the EPF of the account holder.

It’s important to note that if your account remains inactive (no contribution is made) for three years, the money will cease to earn any interest.

In the past several decades, the interest rate has ranged from 8-12 % of the balance maintained in the fund. The table given below shows the interest rates over the years:

|

EPF Interest Rates |

|

|

Year |

Avg Rates (%) p.a |

| 1970-80 | 6.90% |

| 1980-90 | 10.31% |

| 1990-00 | 12.00% |

| 2000-10 | 9.15% |

| 2010-16 | 8.75% |

EPF Withdrawals

Period of investment is usually up to resignation, retirement or death – whichever is earlier. However, premature withdrawals are available under special circumstances (e.g. expenses for marriage, education or medical emergencies, settling abroad, repaying housing loans, paying the costs of alterations/repairs to your existing home). If you’ve completed 7 years of service, you can withdraw 50% of your EPF contribution – up to 3 times in your working life.

Tax Benefits

The employer contribution to your EPF is tax-free and your contribution is tax-deductible under Section 80C of the Income Tax Act. The money you invest, the interest earned and eventually withdraw after the mandatory specified period are exempt from income tax.

Online Access

All your EPF details are available on the EPF India website and you can access your EPF details online with your EPF account number. For more information, check out the website www.epfindia.nic.in

Conclusion

EPF offers you a risk-free, sovereign-secured investment for your retirement that no other AAA-rated product will provide. You should consider it even at current rates.

For The Year 2016

For the year 2016, EPF is one of the best debt investment options, since all other debt funds like PPF, Post Office investments and bank FD rates have come down between 50 bps to 100 bps. However, EPF rates are in the 8.8% range. Following are some of the debt interest rates as of today which normally compare with PF.

|

Product |

Rate |

|

Provident Fund (PF) |

8.80% |

|

Public Provident Fund (PPF) |

8.10% |

|

Monthly Income Scheme – Post Office* |

7.80% |

| National Savings Certificate (NSC) 5 Year |

8.10% |

* Post Office scheme rates change every quarter as declared by the Government.

Source: indiapost.gov.in

What is 80 ccd 1b as per Financial year 2016-17 . Can the mandatory deduction from salary be shown in 80 ccd 1b i.e. 10% of the basic.

Hi Pinky,

Under Section 80CCD(1B), you can claim a deduction for your voluntary contribution to the National Pension Scheme (NPS) of up to Rs. 50,000. This section is not related to mandatory deduction of salary.

Cheers,

Team BankBazaar