Both gold and Mutual Funds are great investments, but which one is better? One needs to do some data crunching to find out.

As you might already know, in India, gold is preferred over Mutual Funds. The typical Indian mindset is such that any marriage or for that matter, any Indian festival, is incomplete without gold. It’s an age-old practice of ours to buy gold jewellery on auspicious occasions. This is often saved as an heirloom and passed on to the next generation. Children today, however, have a mind of their own. They would spend that money on experiences or other assets rather than locking it all up in jewellery which might never see the light of the day. That’s the reason why Mutual Fund investments are becoming popular in our country.

Consider this: Equity Mutual Funds (including Equity Linked Savings Schemes) witnessed the highest ever monthly inflow of Rs. 20,362 crore in August this year. This is a year-on-year increase of over 200%! Also, the number of Mutual Fund folios were at a phenomenal 6 crores at the end of August 2017. Convinced that people have started looking at Mutual Funds?

Additional Reading: Mutual Funds: Should You Take The Lumpsum Route For Good Returns?

What about those in rural areas? Data shows that investors living in towns other than the top 15 cities account for close to 18% of the total Assets Under Management (AUM) of the Mutual Fund industry. Isn’t that fantastic?

Now, do Mutual Funds score over gold? There are actually many points in favour of Mutual Funds. Let’s do some analysis.

The returns

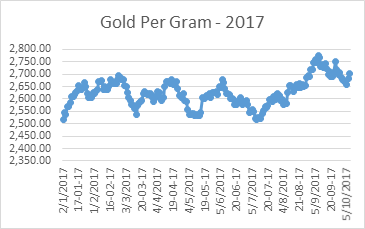

According to Bloomberg data, gold has given an annualised return of 5.5% in the last 10 years. This is much lower than even returns from debt Mutual Funds. What about returns in the last 5 years? It’s a negative 10% for gold. How has gold done this year? Look at the chart below. Gold has been extremely volatile this year and has given a year-to-date return of just about 7%. Not so great, agree?

Why hasn’t gold rallied this year? Data from the World Gold Council shows that investment demand for gold has fallen by 14% to 2,000 tonnes in the first half of 2017. This is the lowest in about 8 years. No wonder gold prices have not risen much. Also, gold prices are dependent on a number of factors other than demand and supply. This includes the geopolitical environment, the demand for US dollar and how the Indian rupee is doing. So, we can say that gold prices are not exactly predictable.

Additional Reading: How Many Mutual Funds Is Too Many?

What about Mutual Funds? The best Mutual Fund in the equity category has given an annualised return of over 30% in the past 5 years. The average annual return from equity Mutual Funds has been 25% for the past 5 years. What about debt funds? The best fund has returned an average of 11.6% in the past 5 years. The category average stands at 8.77%. Aren’t these returns much better than those from gold? The below table lists some of the best Mutual Funds that have performed well in the past.

| Fund Name | Category | 3 year return (annualised) | 5 year return (annualised) |

| ICICI Prudential Long Term Fund | Debt | 11.66% | 11.63% |

| SBI Small & Midcap Fund | Equity | 33.53% | 29.18% |

| Tata Retirement Savings Fund | Hybrid | 19.84% | 17.89% |

| Axis Long Term Equity Fund | Tax Saving | 22.32% | 14.95% |

The liquidity

When you buy an asset, you should be able to sell it quickly for a much higher price. Is this possible with gold?

People fail to understand that gold jewellery is not 100% pure gold and is prone to damage. So when it is sold, it depends on the jeweller buying it to decide the value of the jewellery. Even if you exchange it at the same jeweller from whom you bought it, it might not fetch as much as you would have paid due to making charges, wastage and other ‘non-value adding’ charges while buying it. So, exchanging or selling jewellery might not be profitable. Jewellery also goes out of fashion over time. The most important point to udnerstand is that buying jewellery is more of consumption rather than an investment as jewellery depreciates over time.

Additional Reading: What’s BankBazaar’s CEO Saying About Mutual Funds?

You can sell your Mutual Funds any time and get the money within a day or two. Some funds don’t even charge an exit load if you hold them for a few months or a year. The best part is that the redemption amount is credited directly to your bank account. If you hold equity Mutual Funds for more than a year, you don’t need to pay capital gains tax. What about debt funds? Hold them for 3 years and get indexation benefit. Another advantage is that, unlike gold, you don’t need to pay wealth tax for Mutual Funds. And you, of course, don’t need to worry about storing your Mutual Funds. They remain safe in electronic form. For gold, you need to keep hunting for that bank locker whose charges might leave a hole in your pocket. We can say that Mutual Funds are easy to invest in, provide good liquidity, have no storage hassles and are not subject to high taxes.

So, this festive season, pick up some Mutual Funds instead of gold. We are sure you will reap good returns in the long run.