Received your first salary? Congratulations! Resist the urge to splurge. Instead, a disciplined financial approach from your first pay onwards itself will work wonders in the long run. Here’s what to do.

Receiving your first-ever pay cheque is a proud moment for most of us. It marks the first clear milestone in adulting. While the feeling is quite exhilarating – the flush of financial independence and a sense of accomplishment – resist the urge to splurge. Sure, you’ll probably have a wish list a mile long for when you make your own money and don’t have to depend on your parents. While you may not be answerable to anyone – afterall, your money is your money alone – you do have a responsibility to yourself. And that needs to start with that very first pay cheque.

Additional Reading: Deciphering Your Salary Slip

Here’s what we recommend you do when you receive your first salary:

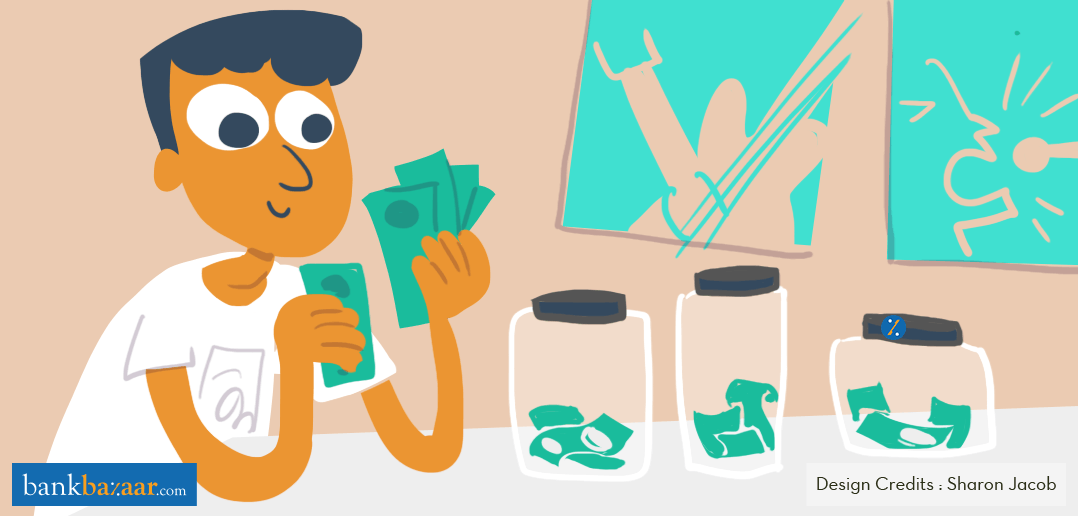

The 50-30-20 Plan

If you’re confused about exactly how much to save and how much to spend, try the 50-30-20 plan. This means 50% towards basic necessities, 30% towards miscellaneous expenses and 20% towards savings and investments.

The Bare Necessities

Set aside 50% of your pay to take care of necessities like household expenses, utility bills, food, transport, rent, an allowance for your parents and so on – essentially, your living expenses.

It is important to plan this, otherwise you will be surprised how quickly your salary will evaporate and you won’t even have much of a clue how that happened. The worst position to put yourself in is to be living from pay cheque to pay cheque.

Discretionary Spending

30% of your pay would go towards discretionary spending. You should reward yourself for your hard work so you can spend this on leisure activities or certain indulgences. Perhaps you want to take up a weekend class or an online course or kayaking or spruce up your wardrobe to make a great impression at work? Those expenses would come out of this 30% quota.

Savings & Investments

The remaining 20% should go into savings and investments. Resist the urge to keep money parked in your savings account – money lying idle in your savings account will earn very little interest. Instead, channel this towards other savings instruments and investment vehicles depending on your risk appetite.

- Build a contingency fund that covers at least three to six months’ worth of expenses so you’ll have a safety net in case of unforeseen events like a medical emergency or job loss, etc.

- Look to grow your money. If you are completely risk averse, consider putting your money into fixed deposits, recurring deposits, post-office savings or sovereign gold bonds. If you have more of an appetite for risk – in which case your opportunity for higher returns increases – consider an SIP of as little as Rs. 100 a month to invest in equities, bonds and other classes of assets. Diversify your portfolio, choosing between liquid, hybrid and multi-cap funds depending on your risk appetite, investment horizon and financial milestones.

- Finally, don’t ignore retirement savings and insurance. Invest in a good pension scheme from Day 1 and you’ll thank yourself one day when you hang up your work boots. You can get a tax-free maturity amount as well as a regular income to see you comfortably through your retirement years. Take life insurance and health insurance policies so that both you and your dependents are covered – don’t take these policies simply to reduce tax. Ensure you have a decent sum assured.

Additional Reading: Using Discipline to Formulate a Good Financial Plan

And there you have it – quite a simple plan to follow. Of course, as your salary increases and financial commitments increase, it would be a good idea to rope in a good financial advisor to help you manage your money better and optimise your returns. The 50-30-20 plan will need to be adjusted depending on your priorities in life as time progresses.

It’s also a good idea to get a Credit Card and start building your credit history. A good credit repayment history, credit utilisation ratio and sizeable age of accounts will stand you in good stead when you are in need of additional lines of credit later in life – for e.g. a Home Loan, Car Loan or Personal Loan. Once you have started your credit journey, always remember to check your Credit Score regularly.

Ready to get your first-ever Credit Card? Simply click the button below. Choose from a range of lifetime-free cards that are high on rewards and cashback for maximum savings.