Credit application rejected despite you maintaining a good Credit Score? Chances are you have a bad debt-to-income ratio!

So, you’ve just checked your Credit Score, and it’s pretty good! You’re thrilled about it and you confidently apply for a Home Loan thinking you’ll breeze through the process with your 800+ score. However, to your surprise, your application is rejected. What could be the reason? Well, it’s probably your debt-to-income ratio that’s caused a problem here.

Just like how you should take care of your Credit Score, you should also keep a keen eye on your debt-to-income ratio if you’re looking to get your credit applications approved easily by lenders.

Understanding Debt-to-Income Ratio

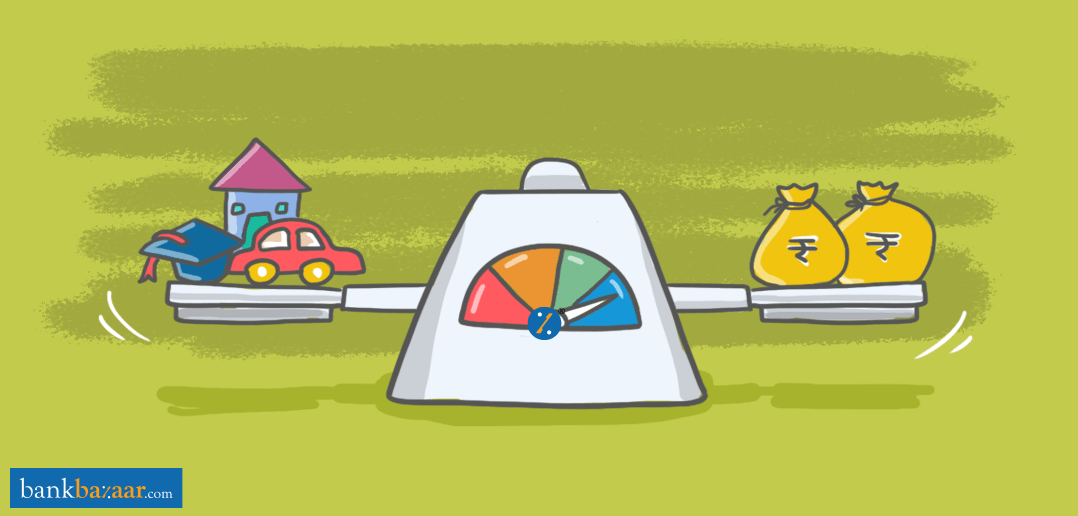

Basically, when you total up all your monthly debts, like your Credit Card payments and loans, and divide this number by your net monthly income, you get your debt-to-income ratio. Debt-to-income Ratio, or DTI, helps banks gauge how much additional debt you can take on based on your present situation.

If you just checked your ratio, and it’s pretty high, don’t rejoice. Remember, in this case the lower the better. A low DTI is proof that you have a good balance between your debts and your income.

Gotcha! So do banks have a limit of sorts for this ratio?

Yes, usually banks have a threshold limit of 40%. Anything beyond that can be perceived as risky business.

How come I have a good Credit Score despite a high DTI?

That’s because your Credit Score is simply not affected by this ratio. It has more to do with how your loans and other credit products were serviced in the past, and nothing to do with your future capability to handle more.

What do I need to do to get a better DTI in the future?

We’re so glad you asked. In this article we’ve broken DTI patterns into three common brackets. Based on where you stand, you can follow our suggestions to up your DTI game in the future. Sounds good? Let’s go!

Below 35% – Woohoo! You’re a rockstar

If your DTI falls within this category, you’ve got your finances sorted. You probably have sufficient money left over even after your bills are paid off. Banks will love your ratio. It’s safe to say that you don’t need much advice as of now – just do what you’ve been doing!

36% – 40% – Not bad, but not great either

You’re probably dealing with your debts just fine, but there’s room for improvement when it comes to your DTI. You can try and work out a little cushion of money for emergency situations by keeping your debt in control. A hike in your income can also help you achieve this.

Additional Reading: Women! Here’s How to Boost Your Income

41% – 100% – Your DTI needs a makeover

If you identify with this category, chances are your debts are eating up a major chunk of your monthly income. There are two reasons to improve your DTI at this point.

Firstly, who would ever say no to some peace of mind? Improving your DTI by better managing your income and spends will surely give you some peace of mind knowing you have some money to fall back on during emergencies.

Additional Reading: Smart And Easy Tips to Get Out of Debt

Secondly, you may want to give lenders some peace of mind as well while they go through your application. As we mentioned earlier, even if you happen to have a desirable Credit Score, banks may still turn you down because of a high DTI. This can be even more heart-breaking than a rejection due to a bad Credit Score, because a good score sort of raises your hopes of a clean, smooth approval. A bad DTI, on the other hand, brings you all the way down from cloud nine and leaves you utterly disappointed.

Not to worry though. You can certainly give your DTI a facelift by following the above suggestions.

Additional Reading: Stuck In Debt? Here’s How To Get Out Of It!

All it takes is some smart money management

As with most things, the key to a more favourable DTI lies in getting your basic finances right. For starters, you can chart out how much money you’re left with at the end of every month. Make a note of the balance amount over a few months. That’ll help you zero in on a well-rounded average. Now, once you have this number, you can analyse how you can gradually bring this up by making little changes in your spending style.

Additional Reading: 7 Must-Have Money Management Apps to Track Your Expenses

Nowadays, money management has become simpler than ever especially with the incredible array of tools at your fingertips. If you’re looking for some fantastic financial products, you’ve come to the right place.